Many individuals who need quick access to cash but do not qualify for traditional bank loans due to bad credit or other financial challenges use payday loans. They provide temporary relief for people in need, but many criticize them for being expensive in the long run. There are significant fees and costs that payday loan borrowers must know before deciding to get a loan. The following blog post explores the various fees associated with online payday loans and how they impact borrowers’ finances.

Summary

One of the key drawbacks of payday loans is their high loan interest rates, leading to a potential financial crisis for the borrowers.Payday loan lenders often require proof of income to ensure borrowers can repay the loan. By understanding the fees and costs associated with these loans, borrowers can make informed decisions about whether or not a payday loan is the best solution for their financial situation.

- Payday loans are short-term, high-interest loans due on the borrower’s next payday and are popular among people with poor credit who need quick cash. They often have a high Annual Percentage Rate (APR), contributing to their expensive nature.

- Payday loan laws vary by state, and some states have prohibited payday lending altogether or have set strict regulations to protect consumers.

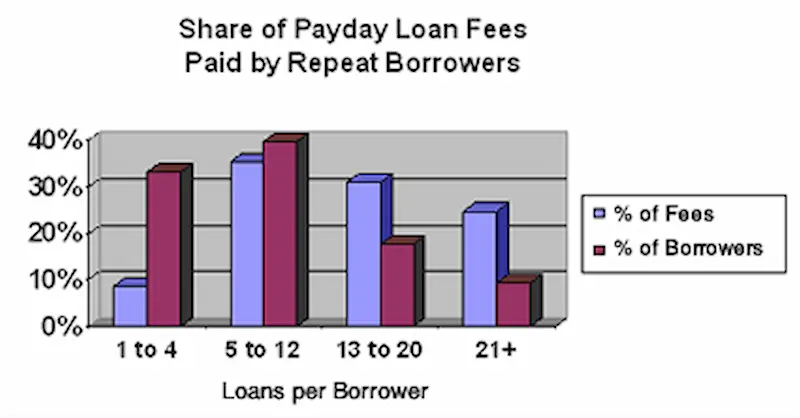

- Payday loans have significant fees and interest rates that quickly add up, leaving borrowers in even worse financial situations, affecting their financial health.

- Fees associated with payday loans include origination fees, late payment fees, prepayment penalties, and overdraft fees if funds are unavailable at the time of repayment. The repayment terms can also differ across lenders.

- Online payday lenders should be reviewed carefully to ensure their legitimacy and avoid scams targeting desperate borrowers.

- Late payment fees, processing fees, and interest rates make payday loans even more expensive if borrowers miss payments or cannot repay on time, leading to an increased outstanding balance.

- Borrowers must carefully examine all fees and costs, including the annual interest rate, before deciding to get a payday loan and only apply if they are confident they can repay on time.

- Creating a budget, exploring other borrowing options, and seeking financial counseling are ways to avoid the need for expensive payday loans.

Understanding The Basics Of A Payday Loan

Payday loans are short-term, high-interest loans due on the borrower’s next payday. They have gained popularity in recent years as a way for individuals with poor credit to obtain quick cash when they need it most. But payday loans have significant fees and interest rates that quickly add up, leaving borrowers in even worse financial situations.

The fees commonly associated with payday loans include origination fees, late payment fees, and prepayment penalties. Many lenders require borrowers to provide access to their bank accounts or post-dated checks as collateral, which results in overdraft fees if funds are not available at the time of repayment. Consumers should examine all the costs associated with payday loans before deciding to get one and consider other loan options that may suit their needs.

One alternative to payday loans is setting up an emergency fund to cover unexpected expenses, which can help avoid the need for high-interest loans in the first place. Additionally, borrowers should be aware of the regulation of payday loans in their area, as some jurisdictions have strict rules limiting interest rates and fees.

What Makes A Payday Loan Expensive?

When evaluating the cost of a payday loan, it’s important to consider not only the interest rate but also fees like origination fees, late payment fees, and prepayment penalties. The monthly payment can quickly become unmanageable, especially if the borrower is already experiencing financial difficulties. Understanding the terms of a loan agreement before signing is essential to avoid further financial problems.

Payday loans become very expensive if the borrower misses their payments or cannot repay them on time. Many borrowers, in such cases, choose to roll over the loan by paying only the finance charge and extending the loan term. But extra fees and interest are added when a loan is rolled over, making the loan even more expensive. Borrowers need to face certain additional finance chargess like application fees, late payment fees, processing fees, loan origination charges, and interest rates. Furthermore, knowing loan rollover fees and understanding the loan terms on an annual percentage rate basis is crucial. Considering alternative solutions like payday alternatives is advisable, especially when one’s monthly income does not suffice to cover the loan balance.

Application Fees

Application fees are fees that payday lenders charge borrowers when they apply for a loan. The fees vary depending on the lender and the state in which the borrower resides. The application fee is a flat fee in certain cases, while it is a percentage of the loan amount in others. It’s best to note that application fees are unnecessary for payday loans.

Certain lenders offer loans with no check fee or application fee, while others waive the fee for certain customers or under certain circumstances. Application fees seem small but add up quickly, especially if a borrower applies for multiple loans. Borrowers must examine the application fee’s cost when applying for a payday loan. They must only apply if they can repay the loan and all associated fees on time. It is also important for borrowers to carefully read the loan contract and understand the overall fee for loans and conditions to ensure they make affordable payments.

Late Payment Fees

Late payment fees are fees that payday lenders charge borrowers when they cannot make payments on time for their loans on time. Late payment fees are flat expenditures added to the amount owed if the loan is late. There’s no exact amount of late payment fees because they vary depending on the lender and the state in which the borrower resides. To avoid unaffordable payments and additional fees, it’s essential to ensure you repay the loan within the provided schedule and during the lender’s business day.

Late payment fees make a payday loan even more expensive. For example, a lender charges a late payment fee of $20 if the borrower cannot repay the loan on time. Borrowers who cannot repay their type of loan on time must contact their lender to discuss their options. Certain lenders are open to working out a payment plan or extending the loan term to help the borrower avoid late payment fees and ensure access to repayment cash.

Processing Fees

Processing fees, which are part of the standards for loans, are a percentage of the loan amount and vary depending on the lender and the state in which the borrower resides. Many lenders charge a flat processing fee, while others waive the cost for certain customers or under certain circumstances. It’s important to understand the loan maximums and various types of loans available before deciding.

Processing fees cover other expenses incurred by the lender, such as credit checks, background checks, and administrative costs. Processing fees add up quickly and make a payday loan even more expensive. For example, the borrower must pay a processing fee of $25 if a lender charges a processing fee of 5% on a $500 loan. Getting multiple additional payday loans makes processing fees a significant expense.

Interest Rates

Interest rates are another key factor to assess when getting a payday loan. Payday lenders charge very high-interest rates, ranging from 300% to 500% or more, according to Consumer Financial Protection Bureau. The rates vary depending on the lender and the state in which the borrower resides. Average payday loan borrower who fails to meet the requirements and the due date for repayment of a loan incurs added fees and interest charges, sometimes even a fee in excess.

When comparing financial products such as personal loans, it’s essential to know the interest rates, fees, and other expenses involved. Payday loans typically have higher fees than other loans, owing to their higher annual interest percentage rate. The consumer protection laws governing payday loans vary from state to state, affecting the maximum interest rate charged and any late payment fees.

State Maximum Interest Rate (%) Late Payment Fee Annual Interest Percentage Rate $500 Loan for 30 Days Total Cost

California 460 $15 $587.50 $687.50

Florida 304 $25 $567.57 $667.57

The table shows the maximum interest rates and late payment fees charged by payday lenders in California and Florida. It includes the total cost of borrowing $500 for 30 days, including the principal and interest charges.

Origination Fees

Lenders charge origination fees to cover the administrative costs of processing a small, short-term loan and vary depending on the loan servicers. They are a percentage of the loan amount and are deducted upfront or added to the total balance that the borrower owes. It’s best to note that the fees significantly increase the overall cost of borrowing, including Cash Advances. People must check them before deciding if a payday loan is the right solution. The basic loan process provides easier access to money for urgent needs, but it’s important to consider the loan duration limit and the potential amounts of money borrowed.

Here are some statistics on fees associated with payday loans:

| Statistic | Value |

|---|---|

| Average payday loan fee | $15 per $100 borrowed |

| Average payday loan borrower pays $520 in fees over the course of a year | Yes |

How To Avoid Having An Expensive Payday Loan

Payday loans don’t have to be expensive. There are several ways to avoid fees and expensive payday loans. Listed below are the steps to avoid an expensive payday loan. One key aspect is properly managing your monthly expenses and seeking advice from financial experts. Consider alternative loans such as the safest loans available, and avoid relying heavily on cash advance loans. Moreover, it is important to stop living paycheck to paycheck and take control of your personal finances.

- Create a budget. Carefully managing expenses and setting aside savings for emergencies allow borrowers to avoid needing short-term loans altogether. Creating and sticking to a budget helps borrowers avoid needing a payday loan. Incorporate a cycle of bills to help monitor expenses and make timelier payments. Also, consider signing up for direct deposit to ensure funds are readily available when needed.

- Explore other options. Other options are available for borrowing money, such as getting a small loan from a credit union, using a credit card with a lower interest rate, or borrowing from friends or family. Look into alternative lending sources and alternative funding sources for better deals on loan terms. Research lower-cost installment loans or cost loans with better interest rates that work for your situation.

- Seek financial assistance. Borrowers struggling with debt or other financial issues must seek assistance from a nonprofit credit counseling agency. The agencies provide free or low-cost advice and assistance with managing debt, creating a budget, and improving your financial situation. Feel free to consult them about business hours for optimal assistance.

- Use alternative financial services. There are alternative financial services, such as community development financial institutions (CDFIs) and online lenders, that offer small loans with more affordable rates and fees than traditional payday lenders. By choosing these services, borrowers can save money and apply for loans with better terms than payday loans.

Conclusion

Payday loans offer a quick solution for people needing cash but have high fees and interest rates that make them expensive in the long run. Payday loans have origination fees, late payment fees, processing fees, and high-interest rates. Borrowers need to understand all the associated costs before getting a payday loan.

Creating a budget and exploring other borrowing options, such as small loans from credit unions or using a credit card with lower interest rates, help avoid the need for payday loans altogether. It is necessary to know that payday loans leave borrowers in even worse financial situations if they cannot repay the loan on time, leading to added fees and charges.

Frequently Asked Questions

What is the typical interest rate for payday loans, and how does it compare to other types of loans?

Payday loans typically have 400-600% APR interest rates, much higher than rates for personal loans, student loans, mortgages, and credit cards which are usually under 30% APR.

Are there any upfront fees or hidden charges associated with payday loans that borrowers should be aware of?

Payday loans often have origination fees of $10-$30 per $100 borrowed plus hidden costs like database fees or prepayment penalties. Read terms carefully.

Can you explain the APR (Annual Percentage Rate) for payday loans and how it affects the overall cost of borrowing?

Payday loan APRs can exceed 500% or more. This extremely high rate, applied to a 2-week loan, leads to overall borrowing costs that are very expensive relative to principal.

Are there any late payment fees or penalties if I can’t repay my payday loan on time?

Yes, late fees are common around 5-10% of the overdue payment. Defaulting can lead to collection costs, bank penalties, loan renewals with added fees, and wage garnishment in some cases.

What regulations or laws govern the fees and charges imposed by payday lenders, and how can borrowers protect themselves from predatory lending practices?

States regulate payday lenders, capping rates and fees. Know your state’s laws. The CFPB also oversees some practices nationally. Research thoroughly before borrowing.