Many people find themselves in need of quick cash for unexpected expenses. They usually have strict eligibility criteria that make it difficult for individuals to qualify, while traditional banks and credit unions offer loans. Payday lenders have emerged as an alternative option for individuals who need help meeting the requirements of banks or credit unions. The payday lending industry has faced scrutiny due to high-interest rates and potential predatory practices.

Loan Approval Process

The loan approval process varies significantly between different types of lenders. Payday lenders, for example, usually operate differently from traditional banks and credit unions regarding their loan approval process.

Listed below are the factors for the loan approval.

- Speedy Processing Time

The most significant difference between payday lenders and traditional banks or credit unions is the speed of loan application processing. Payday lenders approve and disburse funds on the same day, whereas banks or credit unions take several weeks to approve loan applications. The process’s quick turnaround time especially appeals to borrowers who require funds urgently. - Minimal Documentation Requirements

Payday lenders have minimal documentation requirements compared to banks or credit unions. Traditional financial institutions commonly require extensive documentation, such as proof of income, tax returns, and bank statements. Many payday lenders accept online applications with minimal documentation requirements, which are convenient for borrowers who cannot produce extensive documentation. - Higher Interest Rates

Payday loans tend to have higher interest rates than traditional loans, which is the cost associated with the convenience and quick processing time provided by payday lenders. The process of payday lending often results in borrowers paying significantly more over time than they would with a traditional loan. Comparing interest rates and fees from different lenders before selecting a loan product is essential. - Collateral Requirements

Payday lenders require larger loans, while traditional banks or credit unions usually do not require collateral for loan approval. Collateral is an asset that a borrower pledges to the lender as security for the loan. In the case of non-repayment, the lender seizes the asset to recover the loan amount. The process is a necessary deliberation for borrowers who need to have collateral to pledge.

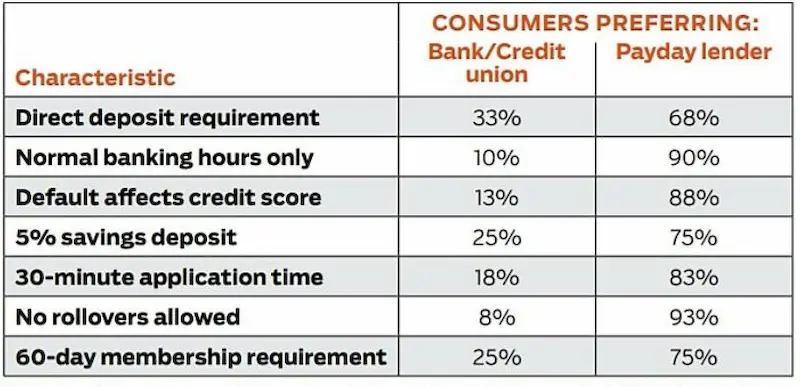

Below are some statistics about payday lenders that differ from banks and credit unions:

| Feature | Payday Lenders | Banks/Credit Unions |

|---|---|---|

| Interest rates | Typically much higher | Typically lower |

| Fees | Typically charge a number of fees | Typically do not charge as many fees |

| Term length | Typically short-term, with terms of 14 to 30 days | Typically longer-term, with terms of 6 months to 5 years |

| Repayment method | Typically repaid by having the lender withdraw the loan amount from the borrower’s checking account on their next payday | Typically repaid by having the borrower make monthly payments |

| Accessibility | Often more accessible to borrowers with poor credit | Typically require borrowers to have good credit in order to qualify for a loan |

Repayment Terms And Options

Payday lenders differ from banks or credit unions in repayment terms and options. Listed below are important considerations for repayment terms and options.

- Online Applications

The primary loan application method for payday lenders is online applications, which is a significant convenience for borrowers. It allows them to apply for a loan without visiting a physical location, saving time and effort. - Shorter Repayment Periods

Payday loans commonly have shorter repayment periods than traditional bank loans or lines of credit. Most payday loans require full payment within two weeks to one month. Borrowers must assess their financial situation and ability to repay the loan in the given timeframe before applying for a payday loan. - Rollover Option

Payday lenders offer a rollover option that extends the borrower’s repayment period and increases interest rates and fees. It is necessary to assess the cost of extending the repayment period before opting for a rollover option. - Grace Periods

Payday loans include grace periods before late fees accrue, but others do not. The lender grants a grace period to allow the borrower to pay without incurring late fees. - Prepayment Penalties

Prepayment penalties are rare among payday lenders as they encourage early repayment to avoid more interest charges. Borrowers save money by making early payments and must check with the lender to guarantee no prepayment penalties exist. - Automatic Payments

Automatic payments are set up through the lender to guarantee timely repayments. The process option provides convenience and peace of mind for borrowers who want to receive all payment deadlines.

Credit Checks And Requirements

Payday lenders are known for their relaxed credit requirements compared to traditional banks and credit unions. Payday lenders do not have strict criteria that borrowers must meet with a good credit score and collateral options in exchange for loans.

Financial institutions, at the same time, require extensive background checks. Many offer no-credit-check loans as an alternative solution for borrowers with bad or no credit history. The alternatives do not mean that payday lenders don’t have any requirements at all. They still verify the borrower’s income through pay stubs or bank statements to guarantee they repay the loan on time.

They still have specific guidelines to protect themselves from potential losses due to non-payment of loans by borrowers, while payday lenders have different requirements than banks and credit unions. Ask for references or proof of residency before approving a loan application. Payday lenders offer collateral options such as car titles or valuables as security in case the borrower fails to repay the loan on time.

Payday lenders provide a viable option where other financial institutions decline requests regarding solutions for bad credit customers. The reason behind the process is that payday lenders understand that poor credit only sometimes indicates a lack of trustworthiness in repaying debts.

Poor credit results from circumstances beyond a borrower’s control, such as medical bills or job loss. Payday lenders assess alternative factors when assessing approval for loans, instead of dismissing the process individuals outrightly based on their past mistakes or present situations, making them accessible even when other options seem out of reach.

Consumer Protections And Regulations

State regulations that govern the payday lending industry vary from state to state and have been put in place to protect consumers from predatory practices. Federal regulations, such as the Fair Debt Collection Practices Act and the Truth in Lending Act, provide more protection to consumers and limit the practices of payday lenders.

Payday lenders are not subject to the same regulations as banks and credit unions, such as the Community Reinvestment Act. Payday lenders, as a result, are able to charge higher interest rates and fees than banks and credit unions, making it more difficult for consumers to pay back their loans.

State Regulations

State regulations play a necessary role in the payday lending industry. Each state has its own set of rules and restrictions regarding payday loans, which vary significantly from one another. The state-by-state differences are necessary to assess consumer protections and regulations.

Licensing requirements for lenders differ depending on the state they operate in. States require lenders to obtain licenses before offering loans, while others do not have any licensing requirements. Legal restrictions vary, with states prohibiting certain loan practices, such as automatic rollovers or multiple loans at once.

Maximum loan amounts and rollover limitations are other areas where state regulations come into play. States limit how much borrowers borrow and how usually they roll over their loans if they are not able to repay them on time. Understanding the process of state-specific regulations is necessary for consumers and lenders alike to guarantee that payday loans are offered ethically and responsibly within each jurisdiction.

Federal Regulations

Federal laws and state regulations significantly influence the payday lending industry. Payday lenders must comply with state-specific rules, restrictions, and federal guidelines. Federal regulators aim to balance the needs of the payday lending industry with consumer protection against predatory lending practices.

Federal regulations require payday lenders to offer clear disclosure of loan terms and fees to borrowers, verify a borrower’s ability to repay before granting a loan, and restrict the number of times loans are rolled over to strike a balance between protecting consumers and supporting the payday lending industry.

Argue that more than the process, federal protections are needed to prevent predatory lending practices by unscrupulous lenders. Industry lobbying efforts usually push back against stricter regulations, while consumer advocacy groups work to strengthen them. It is necessary to understand state and federal laws regarding payday loans to guarantee fair treatment for borrowers and responsible practices by lenders.

Availability And Accessibility

Payday lenders are commonly more accessible than traditional banks or credit unions since they offer online loan applications that are completed anytime. Bank loans usually require an in-person visit during business hours.

The process makes payday loans convenient for borrowers with limited free time or living in rural areas far from banking institutions. There are limitations to the accessibility of payday lenders. States have banned them altogether, while others impose restrictions on interest rates or loan amounts. Language barriers make it difficult for non-English-speaking individuals to understand the terms and conditions of their loans.

The required documentation is generally less extensive than a traditional lender needs when applying for a payday loan. Borrowers must provide proof of income and identification but do not need to submit collateral or undergo a credit check. It means borrowers must fully understand the implications of getting such high-interest loans.

The streamlined process seems attractive to borrowers with poor credit histories or low incomes. Physical access to payday lenders is a barrier for individuals. Many payday lending storefronts operate only during standard business hours and must be closer to potential borrowers’ homes or workplaces.

It is necessary for borrowers deliberating payday loans to carefully evaluate all available options before deciding in light of the process factors. Borrowers must carefully assess their high-interest rates and potential for predatory lending practices, although the process loans offer convenience.

Borrowers must guarantee that they fully understand the terms and conditions of their loan agreements before signing anything to avoid falling into debt traps caused by misunderstandings about repayment schedules or fees incurred over time due to late payments.

How Do Payday Loans Work?

Payday loans have been a popular option for borrowers needing emergency funds or people trying to pay off other debts. The interest rates on payday loans are extremely high and are able to quickly add up, making it difficult for borrowers to pay them off. The table below compares payday loan interest rates to other alternatives and provides information on state regulations according to InCharge Debt Solutions.

| Alternative Options | Interest Rates | Pros | Cons |

|---|---|---|---|

| Credit Cards | 15%-30% | Easy to obtain | High-interest rates |

| Debt Management Programs | 8%-10% | Lower interest rates | Requires credit counseling |

| Personal Loans | 14%-35% | Flexible repayment terms | Requires good credit |

| Online Lending | 10%-35% | Quick application process | High-interest rates |

| Payday Loans | 391%-600% | Easy to obtain | Extremely high-interest rates |

Payday loans have an average interest rate of 391%-600%, as shown in the table, which is significantly higher than the interest rates of other alternatives such as credit cards (15%-30%), debt management programs (8%-10%), personal loans (14%-35%), and online lending (10%-35%). They can quickly become difficult to pay off due to the high-interest rates, while payday loans are easy to obtain.

It is necessary to note that state regulations on payday loans vary. Payday loans are banned in 12 states, and 18 states have capped interest rates at 36% on a $300 loan. 45 states and Washington D.C. have caps for $500 loans, but others are relatively high, with a median of 38.5%. Interest rates in Texas go as high as 662% on a $300 borrowed.

Payday loans quickly become a burden due to the high-interest rates while they seem like a quick solution to financial problems. Explore alternative options and know the state regulations before getting a payday loan.

The Bottom Line

Payday lenders differ extensively from banks and credit unions in several aspects, including loan approval, interest rates, and fees, repayment terms and options, credit checks and requirements, consumer protections and regulations, and availability and accessibility.

Payday lenders have a straightforward loan application procedure that allows borrowers to access funds within minutes. On the other hand, banks and credit unions require extensive paperwork for loan approvals. Payday loans attract higher interest rates and fees than traditional lending institutions such as banks or credit unions. Their repayment terms are shorter than borrowers of conventional financial institutions.

Payday lenders do not conduct comprehensive credit checks on borrowers before approving loans; hence, they target customers with poor or no credit history. Banks and credit unions, in contrast, assess an individual’s creditworthiness before granting loans. Payday lenders operate under less stringent regulatory frameworks than banks or credit unions.

The former differs significantly in several ways mentioned above, while payday lenders and traditional financial institutions offer short-term financing solutions to meet consumers’ financial needs. People seeking short-term funding solutions, therefore, must understand the differences in processes to make informed decisions based on their unique circumstances without falling into debt traps created by unscrupulous players in the industry.

Frequently Asked Questions

What is the primary function of payday lenders compared to banks or credit unions?

Payday lenders primarily provide small, short-term loans to borrowers who may not qualify for traditional credit. Banks and credit unions offer a wider range of financial services and lending products. Payday lenders fill a market need, but often charge much higher interest rates than banks.

How do payday lenders determine eligibility for loans, and how does it differ from traditional financial institutions?

Payday lenders generally have fewer eligibility requirements than banks/credit unions. They mainly verify identity, income, and a bank account in good standing. Banks/credit unions check credit scores and debt-to-income ratios more thoroughly before approving loans.

What are the typical interest rates associated with payday loans, and how do they compare to rates offered by banks and credit unions?

Payday loans typically have very high APRs of 400% or more, while interest rates from banks/credit unions are normally below 30% APR for personal loans. The average payday loan rate is over 10 times higher than rates from mainstream lenders.

Are there any regulatory differences between payday lenders and banks or credit unions in terms of consumer protection?

Payday lenders are regulated at the state level and face less strict oversight compared to banks and credit unions, which have federal consumer protection regulations. There are fewer limits on fees and interest rates for payday lenders.

How do the repayment terms and options for payday loans differ from those of traditional banking products?

Payday loans typically have short repayment terms of 2-4 weeks when the borrower’s next paycheck is due. Traditional bank loans have longer terms of months or years with installment payments. Payday loans offer limited options like rollovers with additional fees.