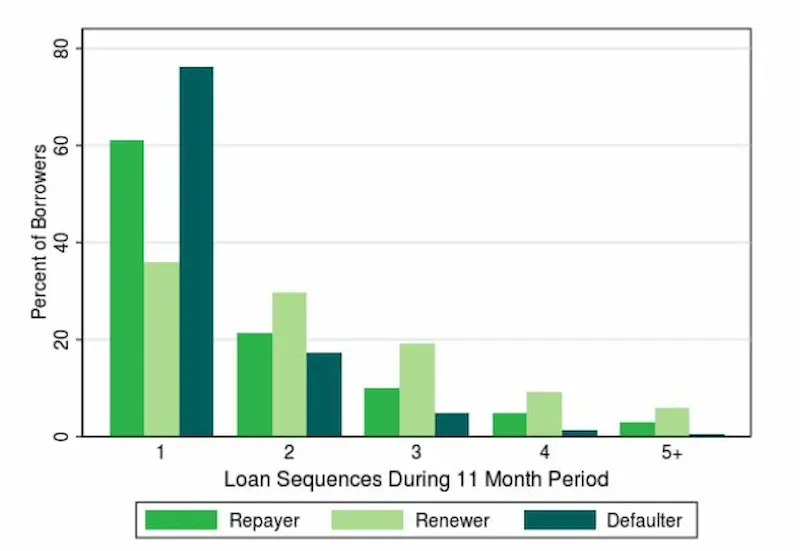

Payday loans provide an accessible way for people to obtain fast cash when they need it urgently. But the ease of accessibility has trapped many individuals into a vicious cycle of debt that is difficult to break out of. People who rely on payday loans usually wonder how many loans they are allowed to have simultaneously. The answer varies depending on state laws and lender policies. The following blog post talks about how many payday loan borrowers are able to get, the effects of having an outstanding payday loan, the role of the payday loan lender, and the applicable payday loan laws.

Summary

- Payday loans provide quick cash for short-term financial needs but lead to a cycle of debt.

- The number of payday loans a borrower is allowed to have is determined by state regulations.

- Lender regulations impact the number of payday loans a borrower has, with certain lenders imposing limits based on creditworthiness or credit history and debt-to-income ratios.

- Two main types of payday loans are short-term loans and installment loans.

- Short-term loans are repaid within two weeks and have high-interest rates and fees, making it risky to get multiple loans simultaneously.

- Installment loans have longer repayment periods and lower interest rates, making them more manageable for borrowers.

- Borrowers must research lenders, check online reviews, compare loan terms, and look out for hidden fees before applying for a payday loan.

- Borrowers must only get loans they afford to repay to avoid falling into a cycle of debt.

State Regulations

Payday loans have become a common financial resource for people who need quick cash. But state regulations play a significant role in determining the number of payday loans an individual is able to obtain. The laws serve as a shield that protects borrowers from falling into debt traps and predatory lending practices.

Certain states allow multiple payday loans at once, while others restrict them to one per borrower or limit the number of rollovers. Some states require online lenders to perform credit checks before approving loan applications. Some individuals might consider additional payday loans as a viable solution to their financial needs, but they must be aware of their state’s regulations and limitations.

It is best for individuals seeking payday loans to understand their state’s regulations and limitations on borrowing to avoid potential financial pitfalls. Doing so helps them make informed decisions about their finances and guarantees responsible borrowing practices without compromising their sense of belonging within society. In this light, exploring alternative loan options can be a helpful step to ensure they meet their financial needs while complying with state laws.

The number of payday loans a borrower can have depends on the state and the lender. For example, a borrower in Alabama must only have one outstanding loan at any time, and this is tracked through a statewide database of all loans taken out.

In Florida, the regulations on the number of payday loans a borrower can have also vary by state law and lender policies. It is essential for borrowers to be aware of the specific guidelines in Florida and check with individual lenders regarding their restrictions on the maximum number of concurrent payday loans allowed.

Lender Regulations

Lender Regulations play a significant role in determining how many payday loans an individual is able to have. The regulations vary from state to state, and lenders must comply to avoid penalties. The annual percentage rate and lending decision process also play a crucial role. The maximum number of payday loans that one is allowed to have at any given time is limited to two or three, depending on the state’s laws.

But certain states do not restrict the number of payday loans that individuals get simultaneously. Many lenders impose limits by assessing an applicant’s creditworthiness or debt-to-income ratio before approving a loan request or providing payday advances.

Types Of Payday Loans

Several types of loans available in the market, and payday loans are just one option among the myriad lending products. Understanding the different types of loans can help borrowers make informed decisions about their borrowing needs and select the most suitable lending product for their current financial situation.

There are various types of payday loans available, and borrowers must decide which one suits their needs to avoid having to get multiple loans simultaneously. It’s essential to consider the type of payday lender, loan interest rates, and the monthly payment amounts. Borrowers are free to choose from short-term and installment payday loans.

Short-Term Loans

Short-term or traditional payday loans are a type of loan designed to be repaid within a short period, usually two weeks. People who need quick cash for emergencies such as medical bills or car repairs use them.

The amount borrowed is usually small and ranges from $100 to $1,000, depending on the lender’s policies and state laws, according to the National Conference of State Legislatures. But it is best to note that getting multiple payday loans simultaneously leads to financial trouble with high loan interest rates and fees. Borrowers must examine their options, including the monthly payment obligations, before deciding how many payday loans they are going to have at one time.

Installment Loans

Installment loans are another option for borrowers and are an alternative to payday loans. These loans have a more extended repayment period and paid back through scheduled payments or installments. The amount borrowed is typically more significant than a short-term loan, and the interest rates may be more favorable. As with any loan, it’s essential to research and compares the type of payday lender and their offered loan interest rates to make an informed decision.

Installment payday loans allow borrowers to repay the loan over an extended period through a series of scheduled payments rather than in a single lump sum payment, like traditional payday loans. The repayment period for installment payday loans ranges from several weeks to several months, depending on the lender and the loan amount.

One advantage of installment payday loans is that they give borrowers more time to repay the loan, which helps make the loan more manageable and affordable. Installment payday loans have lower interest rates than traditional payday loans, which result in significant savings for borrowers over time. The average payday loan’s average interest rate is a sky-high 391% and gets higher than 600%, according to the Federal Reserve Bank of St. Louis.

Considering payday loan alternatives is essential to avoid these high-interest rates. Some other options can be more affordable and less risky for borrowers. Payday loan alternatives include personal loans, credit card cash advances, and borrowing from friends or family.

| Scenario | Installment Payday Loan | Traditional Payday Loan |

|---|---|---|

| Repayment Period | Up to 6 months | 14 days |

| Interest Rate | 25% per month | 391% per year |

| Loan Amount | $1,000 | $500 |

| Total Interest Paid | $250 | $1,955 |

| Total Amount Repaid | $1,250 | $2,455 |

| Advantages | Longer repayment period, lower interest rate, payday alternative | Fast approval, easy to access, payday loan services |

The table compares installment payday loans and traditional payday loans. Installment payday loans have lower interest rates and longer repayment periods, making them more manageable for borrowers and a viable payday alternative. Traditional payday loans offer quick payday loan services with a fast approval process but have high-interest rates, limiting the variety of available financial products.

The table shows the total interest paid and repaid for each scenario. It highlights the advantages of installment payday loans, but borrowers must be cautious and only get loans they afford to repay.

Steps To Take Before Applying For A Payday Loan

The application process for payday loans is usually quick and straightforward, but it varies depending on the lender and the product types of payday loans being sought. A definition of payday loan is a short-term, high-interest loan typically required to be paid back by the borrower’s next paycheck. Payday loan applications are completed online or in person, and borrowers must provide proof of income and identification.

The lender evaluates the borrower’s application and decides to approve the loan and the loan amount. Approved borrowers receive the funds quickly, within a few hours or the next business day, usually via direct deposit. Before receiving the loan, the borrower must agree to the terms in the loan contract.

Research Lenders

Financial crisis can often lead people to seek payday loans, but it’s essential to consider alternatives to payday loans as well. Researching lenders is a key step for borrowers getting a payday loan. Researching lenders allows them to identify reputable payday loan providers who offer fair loan terms and avoid predatory services that try to take advantage of their financial situation during a financial crisis. Here are the steps borrowers must take to research lenders and explore alternatives to payday loans.

- Check online reviews. The best way to determine the reputation of a payday lender is to check online reviews from previous borrowers. Doing so provides insight into the lender’s customer service, loan terms, and overall borrower satisfaction. Look for any mentions of payday debt or issues with online loans.

- Check with state regulators. Certain states regulate payday lenders, and borrowers are free to check with state regulators to determine if a lender is licensed and in good standing. This also helps ensure the lender practices fair loan origination charges and offers a reasonable payment plan.

- Compare loan terms. Borrowers must compare the loan terms, including interest rates, fees, and repayment terms, from multiple lenders to guarantee they are getting the best loan for their situation. Make sure to consider the overall payday debt each loan would entail and any hidden or additional costs.

- Check for hidden fees. Other payday lenders include hidden fees or charges in their loan terms. Borrowers must carefully read the loan terms and ask questions if they need clarification on any fees or charges, such as a high loan origination charge or an unfavorable payment plan.

Understand the Terms And Conditions

Payday loans usually have high-interest rates, fees, and short repayment terms, resulting in a debt cycle for borrowers. Understanding the loan terms allows borrowers to avoid surprises and guarantee they afford to repay the loan on time. They need to understand the consequences of defaulting on a payday loan, which includes legal action and damage to their poor credit score.

Certain payday loans automatically renew if not paid on time, resulting in more fees and interest charges. A common type is the 14-day payday loan, which has a short repayment period. Understanding the loan terms is necessary for borrowers to make informed decisions and avoid the pitfalls of payday loans while maintaining their financial health.

However, borrowers should be aware that having an active payday loan can negatively impact their financial situation, especially regarding credit ratings and borrowing capabilities.

Conclusion

Payday loans provide fast cash but lead to a cycle of debt. The number of obtained payday loans depends on state and lender regulations. Short-term loans are repaid within two weeks, while installment loans over several months. Considering the risks and impacts on one’s financial health, poor credit, and the potential for multiple loan cycles, it’s important for borrowers to thoroughly understand the terms and consequences of payday loans before making a decision.

Installment loans have lower interest rates, but you must use them responsibly. Borrowers with bad credit must research lenders, check online reviews, compare loan terms, and look for hidden fees before getting a cash advance or a payday loan. Making informed decisions about borrowing and paying off your current loan is best to avoid falling into debt traps and maintaining proper time payments.

Frequently Asked Question

Is there a legal limit on the number of payday loans a person can have at once?

Most states don’t specify a legal maximum, but lenders typically limit borrowing to 1-2 loans per customer. Some states limit payday lending to a percentage of income.

What factors determine the maximum number of payday loans a person can take out?

Lending limits depend on state laws, lender policies, and a borrower’s income level and total outstanding loan obligations. Applicant’s credit history also plays a role.

Can I have multiple payday loans from different lenders simultaneously?

Yes, it’s possible to have several concurrent payday loans from different stores or websites, leading to very high cumulative fees and unmanageable repayment. This practice should be avoided.

Are there consequences for exceeding the allowable number of payday loans?

Consequences may include aggressive debt collection, bank account fees, default, continuously rolling over loans with new fees, property liens, and wage garnishment in extreme cases.

How can I responsibly manage multiple payday loans if I need them?

Communicate with lenders, consolidate debt, create a realistic budget, prioritize essential expenses, negotiate alternate payment plans, and pay down highest interest debt first. Avoid relying on payday loans long-term.