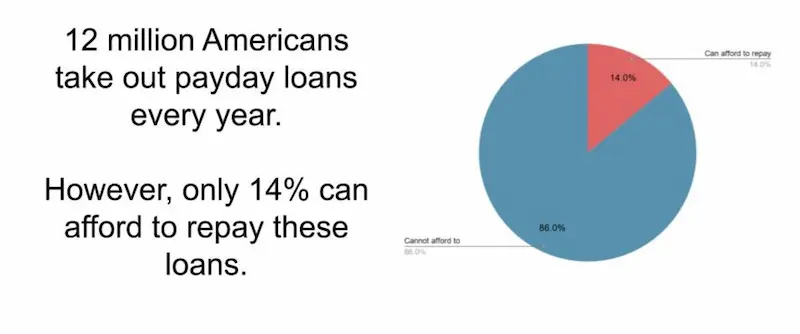

Payday loans are a type of short-term high-interest debt that is due on the borrower’s next payday. These loans are often offered by predatory lenders who exploit vulnerable borrowers. Payday loans are marketed as a quick and easy solution to financial emergencies or unexpected expenses but failing to pay back a payday loan lead to serious consequences.

Each lender has different policies and procedures for dealing with delinquent borrowers and common outcomes that occur if you don’t pay back your high-interest debt. It is necessary to understand what happens next if you cannot repay your payday loan on time. The article explores what happens if you don’t pay a payday loan and how to protect yourself from potential consequences caused by predatory lenders.

Not paying a payday loan has various consequences that negatively impact your credit score and financial standing. The lender charges fees and interest, and if the loan remains unpaid for an extended time, they turn the debt over to a debt collection agency or pursue legal action against you, which leads to wage garnishment, asset seizure, or even court judgments against you. It’s necessary to carefully evaluate the terms of any loan agreement before accepting it and to make timely payments to avoid the consequences.

SUMMARY

- Types of loans vary, but payday loans are short-term high-interest loans due on the borrower’s next payday.

- The APR for payday loans ranges from 391% to more than 521% making them an expensive form of borrowing.

- Not paying a payday loan results in negative consequences that negatively impact credit score and financial standing. Late fees and increased interest rates are common consequences of not paying a payday loan on time. Defaulting on a payday loan damages credit scores, lead to harassment from debt collectors, and results in legal action being taken against the borrower.

- Potential legal action against the borrower includes wage garnishment, seizure of bank accounts, and lawsuits. Careful planning and seeking financial counseling services are necessary to avoid the consequences.

What Are Payday Loans?

The concept of payday loans has existed since ancient times, and only recently have they become more widely available. Payday loans are a type of loan that enables the borrower to receive quick access to cash in exchange for paying a fee. Payday lenders offer short-term advances on paychecks by requiring borrowers to write a post-dated check or authorize an electronic withdrawal from their bank account.

In recent times, online lenders have also become a popular option for obtaining payday loans. These digital platforms allow borrowers to access funds quickly and with minimal hassle.

Payday loans provide an invaluable service as they allow individuals to fulfill basic needs while having limited financial resources, which appeal particularly to people who require immediate funds but need help accessing traditional forms of credit due to bad credit history or lack thereof. Payday loans have little paperwork and no need for collateral, making them much easier for people with few means.

Payday loans do not require any credit checks so long as the borrower demonstrates proof of income, making them one of the most convenient options for unexpected costs such as medical bills or car repairs. Many lenders provide the following:

- Flexible repayment plans.

- Allowing borrowers greater control over how quickly they repay their debt.

- Thus ensuring better budgeting practices.

However, a better financial solution might be worth considering a credit union for lower interest rates and more affordable options like Debt consolidation loans.

Rates and Annual Percentage Rates for Payday Loans?

Payday lenders usually charge interest of $15-$20 for every $100 borrowed. They are calculated on an annual percentage rate basis (APR), the same as used for credit cards, mortgages, auto loans, etc., and APR ranges from 391% to more than 521% for payday loans, according to InCharge. In contrast, a credit union might offer more reasonable rates and Debt consolidation loans to help manage debts more efficiently.

| Loan Amount | Interest Rate | APR |

| $100 | $15 | 391% |

| $100 | $20 | 521% |

| $200 | $30 | 391% |

| $200 | $40 | 521% |

| $500 | $75 | 391% |

| $500 | $100 | 521% |

The table above shows the different loan amounts and interest rates to calculate payday loans’ annual percentage rate (APR). The APR is the total cost of borrowing, including interest and any fees expressed as a percentage of the loan amount. Comparing these loan costs to traditional loans can help make an informed decision.

The table illustrates that payday loans have exorbitant APRs making them a costly form of borrowing. It highlights the importance of understanding the actual cost of borrowing, including fees and interest rates, before getting a loan, especially when compared to traditional loans.

What Are The Dangers Of Not Paying A Payday Loan?

Defaulting on a payday loan has severe consequences. It damages your credit score, leads to continuous harassment from debt collectors, and results in legal action against you. It even causes a bankruptcy in extreme cases. The repercussions of not paying back the borrowed amount with interest seem initially insignificant but accumulate over time. Borrowers find themselves trapped in a cycle of debt that is difficult to break free from without seeking professional help or restructuring their finances as the high-interest rates add up. Payday loans must be paid on time to avoid any unwanted consequences.

Late Fees And Increased Interest Rates

Borrowers must repay their payday loans on time to avoid late fees and increased interest rates. Late fees are charged after a borrower misses a payment deadline, with the amount varying by lender but ranging from $15 to $50 per missed payment. Many lenders increase the interest rate on the loan after it becomes delinquent. The higher rates quickly add up over time, making it even more difficult for borrowers to repay their debt. Borrowers must understand the potential consequences before taking a payday loan and have a plan to repay the loan on time or seek other options if necessary. One way to manage this is by keeping track of their monthly payments to avoid delinquency.

Potential Legal Action

Legal consequences of not paying a payday loan include wage garnishment, deducting money from an individual’s wages to pay off a debt. Wage garnishment is a last resort to recoup unpaid debts, especially if a debt defaults. Potential legal action refers to initiating a lawsuit or legal proceeding against an entity for alleged wrongdoing or breach of contract.

Individuals or organizations must seek legal advice to determine the merits of their case and the potential legal options available before taking legal action. Legal action has significant financial and emotional consequences, so careful planning is necessary. Alternative dispute resolution methods such as mediation or arbitration are determined before resorting to litigation.

Legal Consequences

Failing to pay a payday loan lead to legal consequences. Most states allow lenders to charge late fees and interest rates that quickly accumulate if payments are not made in full and on time. Lenders take legal action against borrowers who default on their loans depending on the state, which means they file a lawsuit and obtain a court order for wage garnishment or bank account seizure.

Borrowers must know the potential legal ramifications of non-payment and seek assistance from financial counseling services if they struggle to make payments. It is necessary to address any outstanding debts promptly to avoid further financial difficulties.

Wage Garnishments

Lenders seek legal action against them in cases where borrowers fail to repay payday loans. The form of legal action that a lender takes is wage garnishment. Wage garnishment means that a portion of the borrower’s paycheck is deducted by their employer and sent directly to the lender until the loan is fully paid off.

The garnished amount depends on state laws but generally ranges from 10-25% of the borrower’s disposable income, which significantly impacts a person’s finances and makes it difficult for them to cover other necessary expenses such as rent or utilities. Borrowers must understand the potential consequences of not repaying payday loans and include alternative options before taking a payday loan.

How To Avoid Payday Loan Trouble?

Creating and following a budget help individuals manage their finances and reduce the likelihood of needing to take a payday loan. Shopping around for the best rates when applying for a payday loan helps consumers save money in the long run.

Payday loans are tempting when you need cash quickly, but they have high-interest rates and fees that are difficult to repay. It’s best to explore other options, such as borrowing from family or friends, using a credit card with a lower interest rate, or seeking assistance from a non-profit credit counselor to avoid payday loan trouble.

Only borrow what you need; repay it on time if you take a payday loan. It’s necessary to read the terms and conditions carefully and understand the fees associated with the loan. Avoid taking multiple loans at once or rolling over the loan, as it leads to a cycle of debt that is difficult to escape.

Establish A Budget

A budget can help you manage your monthly expenses and prioritize debt repayment. Contact a credit counselor to help create a personalized budget for your financial situation. They can also help you evaluate if a debt management plan is a good option for you, where they would negotiate with your creditors and create a repayment plan with lower interest rates and fees. By establishing a budget and enrolling in a debt management plan, you can work towards becoming debt-free and avoid the pitfalls of payday loans.

To avoid payday loan trouble, it is necessary to establish a budget that involves the following:

- Carefully tracking all income and expenses.

- Creating a plan for spending and saving each month.

- Sticking to that plan closely.

Establishing a budget is a necessary step toward financial stability and independence. Individuals must have enough money to cover necessities like rent, utilities, groceries, and transportation without relying on high-interest loans. People can reduce the likelihood of needing to take loans in the future by setting aside funds for unexpected emergencies or expenses.

Shop Around For the Best Rates

Another effective way to avoid payday loan trouble is by shopping around for the best rates. It is tempting to take a loan from the first lender that approves an application which results in paying exorbitant interest rates and fees. Individuals can find one with more reasonable terms and conditions by researching and comparing different lenders, which means lower interest rates, longer repayment periods, or fewer hidden costs. Finding a reputable lender who offers fair loans help people avoid falling into debt traps and improve their financial status.

How To Get Payday Loans?

Payday loans offer an easy and reliable way to get fast cash when needed. No credit check is required, and Same-day loan approvals are ideal for anyone needing emergency funds. No credit check is required making them perfect for people with bad or limited credit. You quickly receive the fast cash you need without hassle or long wait times.

Listed below are the steps on how to get a payday loan.

- Apply for a loan. You must complete a quick and easy online application to apply for the payday loan that best fits your needs. Many payday lenders have streamlined the process so that applications take as little as 10 minutes to complete.

- Submit documentation. The lender requires documentation to verify income and establish creditworthinessOnce you’ve applied. You must provide a copy of your driver’s license, proof of address, or bank statements before the loan is approved. Documents must be ready when applying for fast cash with payday loans.

- Wait for approval. Depending on the lender, it takes several hours to several days to approve your loan application. Payday loans are approved more quickly than traditional bank personal loans since they generally don’t require extensive background checks or credit score assessments.

- Receive funds. You receive the funds from your payday loan in as little as one business day via direct deposit or mailed check, depending on the lender you applied with.

- Repay the loan. Payday loans must be repaid within two weeks after receipt unless other arrangements have been made with the lender beforehand, such as extending the term length or refinancing a balance owed for an extended period at a higher interest.

Here are statistics on how to get payday loans:

| Statistic | Value |

|---|---|

| Loan amount | $100 – $1,000 |

| Interest rate | 400% |

| Repayment period | Next payday |

| Required information | Name, address, Social Security number, checking account, and steady income |

| Risks | High cost, debt trap, and cycle of debt |

| Alternatives | Personal loan, credit card, and government assistance program |

| Tips | Save money in advance, look for other sources of financing, and talk to a financial advisor |

Final Thoughts

Payday loans are a type of high-interest short-term loan that result in serious consequences if not paid back on time. The borrower faces fees, increased interest rates, and potential legal action, such as wage garnishment or asset seizure. Late payments negatively affect the borrower’s credit score making it harder to obtain credit in the future. It’s necessary for borrowers to carefully evaluate the terms of any loan before accepting it and to make timely payments to avoid the consequences. Borrowers can seek financial counseling services if they are struggling to make payments.

Frequently Asked Questions

What are the consequences of not repaying a payday loan on time?

Consequences can include aggressive collections, NSF fees, continuous auto-debit attempts, lawsuits, garnished wages, long-term credit damage, and increased overall repayment costs.

Can you explain the legal actions that can be taken if I fail to pay back a payday loan?

Lenders can sue for repayment, garnish your wages, place liens on property, damage your credit, send accounts to collections, and charge hefty late fees if you default.

How does non-payment of a payday loan impact my credit score and financial future?

Missed payments hurt your score. Defaulting makes repayment and future borrowing more expensive. Wage and asset seizure creates long-term financial struggles.

Are there any alternatives or options available if I can’t afford to repay my payday loan?

You may be able to negotiate an extended repayment plan. Non-profit credit counseling or a debt management plan can also help manage unaffordable payday loan debt.

What steps can I take to negotiate with a payday lender if I’m unable to make my repayment on schedule?

Be proactive, explain your situation and limitations, provide evidence, request an affordable repayment plan in writing, get help from an advocate if needed.