$3000 installment loans online are personal loans repaid in equal monthly installments over a set term. Online lenders offer these loans. They provide quick funding for larger expenses or emergencies. The loan application process is completed online. It includes submitting documentation and receiving loan funds. A $3000 loan is a very common type of personal installment loan.

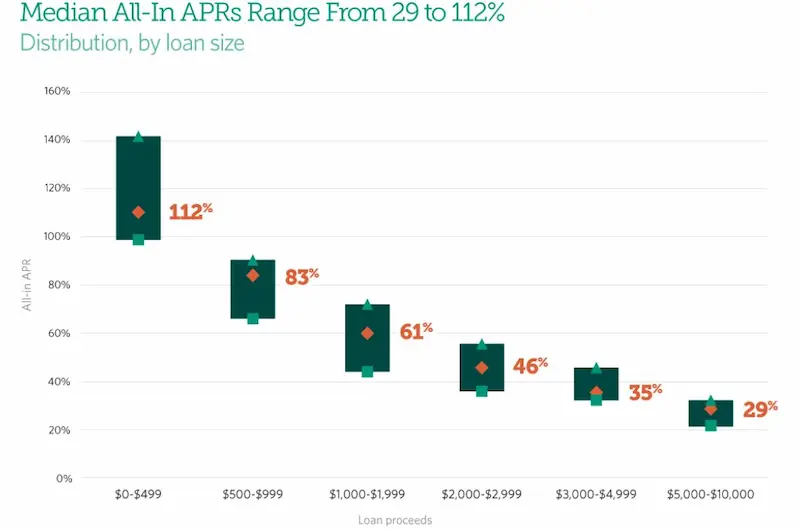

The amount on installment loans varies from $500 (minimum loan amount) to $10,000 (maximum loan amount) dollars. It depends on creditworthiness and employment history. Most installment loan lenders do not perform hard credit checks. They only conduct soft credit checks to see if a borrower qualifies. Soft credit checks do not affect a borrower’s credit score. It offers lower interest rates than payday loans. Lenders expect it back within a few months with interest rates by lending borrowers money. Borrowers must make equal installments every month. Thus, these loans come with flexible terms. Missing an installment loan means a borrower pays extra fees.

How long does it take to get approved?

The best thing about these financial products is that borrowers get approval within minutes. They only need to apply online and leave the rest to the lender. The lender responds within a few minutes. The feedback lets the borrower know if they are approved or not. A 3000-dollar loan is a very common type of personal installment loan. The amount on installment loans usually varies from 500 dollars to 10,000 dollars. It depends on creditworthiness and financial history. However, some lenders, like GreenDayOnline, lend to bad credit borrowers.

How does this kind of loan work?

Installment loans work by allowing borrowers to repay them with equal monthly installments. Each monthly payment depends on many factors. Most borrowers get their loan within one business day after applying. These include the loan term, the interest rate, and borrowed amount.

Listed below are an example of how a $3,000 installment loan might work.

- Borrowers submit their details and apply for it. They must agree to a few things before applying. These include the interest rate, the length of the loan, and any fees associated with the bad credit loan.

- After approval, the lender sends the money in a lump sum within one business day.

- Borrowers must begin making regular payments on the loan over a set period.

- The total loan decreases as borrowers keep making monthly payments. After completing all payments agreed upon between a lender and a borrower, the loan is cleared.

How long does it take to repay the loan?

There is no specific loan term for this personal loan. Terms vary depending on various factors. Some of these are the number of payments to make, the debt-to-income ratio, the credit score, and the interest rate. Suppose a borrower obtains a $3000 installment loan with a 3% interest rate. The borrower accepts to repay the bad credit loan over a three-year term by making monthly installments. In such a case, they must complete 36 payments with installments of $87.11 each. The total loan payment is approximately $3142.96, which contains the interest rates and compound principal. Most websites have a personal loan calculator that borrowers use to confirm their loan costs. They know their potential rates before applying for a loan.

Suppose the borrower opts to take out the same loan for an extended repayment period. The monthly payments are lower. For example, the same loan on a five-year term means lower monthly payments but more interest rates. In case borrowers opt for a shorter period, they make more monthly payments. However, they pay cheaper interest rates. Those with bad credit histories tend to pay more interest rates than those with excellent credit histories.

Are There Monthly Payments?

Yes, installment loans only have monthly payments, which is the main feature of these loans. For $3000, borrowers pay the loan back over 3,6,9, or 12 months. Bad credit score borrowers must know that the loan length determines the interest rates. The longer it takes to repay the loan, the more the interest rate. Borrowers need to find a lender offering competitive interest rates to avoid overpaying for the loan.

Are there advantages and disadvantages associated with this type of loan?

Advantages of installment loans:

- Predictable payments. The best thing about this personal loan is that borrowers know what to pay monthly. It makes it easier for them to budget for the loan.

- They have fixed interest rates. Having a fixed interest rate gives borrowers peace of mind. They know the personal loan rates won’t go up over time. Hence easier to pay.

- It improves credit scores. Some online lenders report payments to the major credit bureaus. Therefore, their records show that they pay off loans on time and improve their credit report.

- Borrowers use it for a variety of purposes. Another advantage is that borrowers use the loan for anything they want. They use them as a debt consolidation loan or credit card debt if they have other debts. Lenders do not decide what the borrower does with the loan unlike other loans like mortgages.

- No credit check. Most online installment loan lenders do not do a hard credit pull and do not need a strong credit limit. They do not check a borrower’s credit file to check their credit score range. It is because they do not have a minimum credit score requirement. Therefore, it does not have an impact on credit scores.

Disadvantages of installment loans:

- They have higher interest rates than some other types of loans. Compared to other loans, like mortgages, installment loans are expensive. Borrowers must know the interest rates before borrowing. They must ensure they make the payments as required by avoiding late payments. They must opt for loans with the lowest interest rates if they are not able to.

- They require collateral. Some types of installment loans need borrowers to provide collateral. Examples of collateral include a car or home. The borrower seizes the collateral if a borrower fails to repay the loan.

- It may not be suitable for short-term borrowing. Suppose a borrower needs a loan for a short-term solution. An installment loan is not the best option. In such a case, consider a short-term loan like a payday loan.

Where can I get a 3000-dollar loan?

Borrowers obtain installment loans from a variety of places. Common installment loan providers include online lenders, credit unions, banks, and peer-to-peer lenders. Requirements and monthly repayment terms for getting the loan depend on the lender. Borrowers looking for a $3000 loan have the following loan options:

- Banks and credit unions: These are some of the most common traditional lending institutions. The best thing about these lenders is that they offer the lowest rates. However, they have stricter eligibility requirements than other lenders. Most credit unions and banks offer interest rate discounts.

- Online lenders: Many online lenders provide installment loans as part of their personal loan offers. These unsecured loans have the easiest loan application process. Most borrowers opt for these lenders as they have easier qualification requirements. However, they come with higher interest rates and annual percentage rates than banks and credit unions.

- Peer-to-peer lending platforms: These are typically platforms that allow people to lend and borrow money from each other. They transact directly without going through any financial institution. The good thing about them is that they come with flexible repayment terms and competitive rates.

As a leading provider of financial solutions, we are proud to extend our services to numerous American states, empowering individuals with accessible options for financial stability. Our commitment to helping individuals with bad credit has led us to establish a strong presence across various states, ensuring that those in need can avail themselves of our $3000 installment loans online. To help you better understand our reach, we have compiled a comprehensive table below, detailing all the American states where our company is actively serving customers. Please refer to the table to discover if your state is included in our coverage, and take advantage of our seamless application process to secure the financial assistance you deserve.

| Alabama | Alaska | Arizona |

| Arkansas | California | Colorado |

| Connecticut | Delaware | District Of Columbia |

| Florida | Georgia | Hawaii |

| Idaho | Illinois | Indiana |

| Iowa | Kansas | Kentucky |

| Louisiana | Maine | Maryland |

| Massachusetts | Michigan | Minnesota |

| Mississippi | Missouri | Montana |

| Nebraska | Nevada | New Hampshire |

| New Jersey | New Mexico | New York |

| North Carolina | North Dakota | Ohio |

| Oklahoma | Oregon | Pennsylvania |

| Rhode Island | South Carolina | South Dakota |

| Tennessee | Texas | Utah |

| Vermont | Virginia | Washington |

| West Virginia | Wisconsin | Wyoming |

Here are statistics on $3,000 installment loans online for bad credit

| Stat | Value |

|---|---|

| Average interest rate | 36% |

| Average term | 36 months |

| Average monthly payment | $92.22 |

| Total interest paid | $970 |

| Borrower demographics | 18-65 years old, employed, with fair to bad credit |

| Loan uses | Unexpected expenses, such as car repairs or medical bills |

Can I obtain an installment loan with a poor credit rating?

Yes, a good credit score helps obtain an installment loan from many online lenders. However, it is not always a requirement. Poor credit history borrowers obtain these loans. Online lenders only perform a soft credit inquiry. Some online lenders offer installment loans designed for borrowers with poor credit scores. They do not require a credit check or consider credit scores as part of their lending decision.

There are several reasons why these lenders do not require a credit score or credit check for on loan. Some lenders use alternative measures of creditworthiness. These include a borrower’s income, employment history, and debt-to-income ratio instead of traditional credit scores.

Other lenders are willing to take on the risk of lending to borrowers with less-than-perfect credit. The lenders lend money to such borrowers if the loan has collateral, or the borrower has a strong track record of making payments.

Lendly loans is a great option for borrowers with poor credit history as they do not require a credit check or consider credit scores as part of their lending decision. Some lenders use alternative measures of creditworthiness, such as a borrower’s income and employment history. Additionally, some lenders are willing to take on the risk of lending to borrowers with less-than-perfect credit if they have collateral or a strong payment history.

Frequently Asked Questions

How can I qualify for a $3000 installment loan online with bad credit?

To qualify with bad credit, focus on verifiable income, long-term employment, minimal existing debt obligations, collateral assets, and meeting high debt-to-income ratio requirements. Also emphasize timely rent/utility bill payments. Having an existing relationship with an online lender helps. Consider a cosigner or meet criteria for bad credit loan guarantee programs if you qualify.

What are the typical interest rates and repayment terms for $3000 installment loans for bad credit online?

A $3000 online installment loan for bad credit typically carries interest rates between 15% – 35% APR depending on specific credit score factors. Loan repayment terms are normally structured over 12-48 months for affordable monthly payments. Shorter terms have higher monthly costs but less overall interest paid over the life of the installment loan.

Are there any reputable online lenders that offer $3000 installment loans for individuals with poor credit?

Some reputable online lenders providing $3000 installment loans for bad credit borrowers include LendingPoint, LendingClub, Prosper, Lightstream, Upstart, Earnest, and Avant. They partner with multiple affiliated banks and financial institutions to fund loans, providing credibility versus lone lenders.

What documents and information do I need to apply for a $3000 bad credit installment loan online?

Required documents and information typically include a government-issued ID, proof of income such as pay stubs or tax returns, residence history, bank account statements, references, Social Security number, employer name and contact details, and any information related to outstanding debts, assets, or collateral that could secure the loan.

What are some alternatives to $3000 installment loans for bad credit that I should consider before applying?

Alternatives to consider include borrowing from family or friends, 401k/pension loans, home equity loans or lines of credit, government aid programs, low interest credit union loans, balance transfer credit cards, and debt management plans through credit counseling to negotiate lower payments on existing debt.