Many people are struggling to make ends meet in today’s uncertain economy. People rely on payday and installment loans to cover their expenses, which quickly become overwhelming due to high-interest loans and fees. Consolidating the loans helps manage debt more effectively by reducing interest rates and fees while simplifying repayment.

The following blog post explores the benefits and drawbacks of consolidating payday and installment loans and high-interest loans and provides tips for successful consolidation. Careful planning is necessary before embarking on this path, as there are better options than consolidation for everyone. Debt management plans could be a more suitable alternative for some individuals.

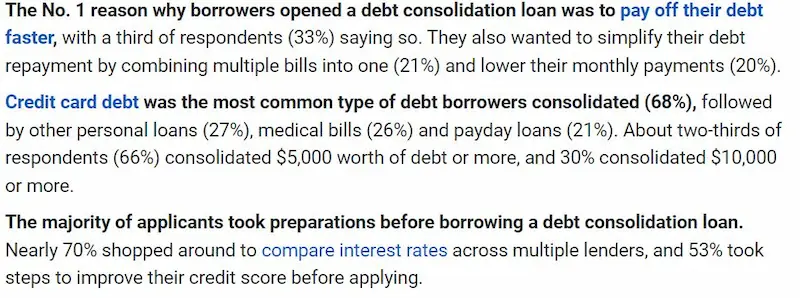

Summary

- Payday and installment loans are short-term loans that people turn to for quick access to funds when they cannot qualify for traditional bank loans.

- Consolidation effectively manages multiple payday and installment loans, simplifies repayment, and potentially reduces interest rates and fees.

- The benefits of consolidation include simplified payments, lower interest rates, reduced monthly payments, improved credit scores, and more flexibility in managing debt.

- Consolidation loans are obtained from banks, credit unions, or other financial institutions and are used to pay off multiple existing debts by combining them into a single loan.

- Borrowers must determine their total amount of debt, check their credit score, compare interest rates and fees, review repayment terms, and accurately fill out the application form.

- The process of applying for a consolidation loan is generally straightforward, and lenders provide feedback regarding the borrower’s eligibility for a consolidated loan.

- Repaying the consolidated loan varies depending on the lender, loan terms, and the borrower’s creditworthiness. Making timely payments and avoiding penalties or late fees is best.

Understanding Payday And Installment Loans

Payday and installment loans are two short-term loans that borrowers turn to in times of financial need. Payday loans, or cash advances, require repayment by the borrower’s next paycheck and usually have high-interest rates. On the other hand, installment loans allow borrowers to repay the loan over a longer period with regular payments but still have high-interest rates.

Both types of loans are helpful for individuals who need quick access to funds but do not qualify for traditional bank loans due to poor credit or lack of collateral. But it is best to understand the terms and conditions of each type of loan before borrowing and think of consolidating multiple payday or installment loans to simplify payment schedules and lower overall costs.

Benefits Of Consolidating Loans

Borrowers currently paying off multiple loans experience challenges, such as high-interest rates, multiple payment due dates, and fees that add up over time. Consolidation is an effective solution for borrowers to simplify their repayment process and potentially reduce their overall interest rates and fees. Listed below are the benefits of using consolidation loans.

- Simplified Payments – Consolidating multiple loans into a single loan simplifies payments, making it easier to manage debt. Borrowers only need to keep track of one debt instead of tracking multiple due dates, payments, and interest rates.

- Lower Interest Rates – Borrowers can secure a lower interest rate, saving them money over the life of the loan.

- Reduced Monthly Payments – Consolidating loans results in lower monthly payments if borrowers secure a lower interest rate or extend the repayment term. It helps ease their financial burden.

- Improved Credit Score – Consolidating loans helps improve a borrower’s credit score, especially if they have multiple high-interest debts. Paying off the debts and consolidating them into a single loan allows borrowers to reduce their credit utilization rate, which improves their credit score.

- Flexibility – Consolidating loans gives borrowers more flexibility in managing their debt. They choose the best repayment terms for them and select a loan that offers features like deferment, forbearance, or prepayment penalties.

Here is a table of statistics about How To Consolidate Payday And Installment Loans:

| Statistic | Value |

|---|---|

| Number of payday loans taken out each year | 12 million |

| Average payday loan amount | $375 |

| Annual percentage rate (APR) for payday loans | 400% |

| Percentage of payday loan borrowers who roll over their loans | 60% |

| Average amount paid in interest and fees by payday loan borrowers over the course of a year | $520 |

| Demographics of payday loan borrowers | Low-income, poor credit scores, unemployed, women, minorities |

| Alternatives to payday loans | Personal loans, credit cards, government assistance programs |

Finding The Right Loan Consolidation Option

Understanding loan consolidation options are necessary when converging payday and installment loans. Borrowers must know what consolidations are and how to get one. Comparing different consolidation solutions helps to determine the best option for an individual’s financial situation.

Understanding Loan Consolidation Options

Consolidation loans are loans used to pay off multiple existing debts, such as credit card balances, personal loans, or other high-interest debts, by combining them into a single loan. Consolidation loans are obtained from banks, credit unions, or other financial institutions.

The primary purpose of consolidation loans is to simplify the repayment process by combining multiple debts into a single monthly payment. They make it easier for borrowers to manage their debts and avoid missing payments, which result in late fees and negatively impact their credit scores.

Consolidation loans help borrowers save money by offering a lower interest rate than the interest rates on their debts. It results in lower monthly payments and an overall reduction in the total amount of interest paid over the life of the loan.

Comparing Consolidation Solutions

Choosing the right consolidation loan is necessary because it saves borrowers money on interest and reduces their monthly payments. Failure to choose the right loan results in higher costs and financial strain. Careful planning and research help borrowers choose the right consolidation loan. Listed below are the steps to compare and pick the right consolidation loan.

- Determine the debt. Borrowers must determine the total amount of debt they want to consolidate. Doing so helps them identify which loans meet their needs and which loan offers might suit them.

- Check the credit score. The borrower’s credit score impacts the interest rate they qualify for, so it’s best to know their score before applying for a consolidation loan. They can perform a credit check by obtaining a free credit report from each of the three major credit bureaus once per year.

- Compare interest rates. Compare the interest rates different lenders offer and choose the loan with the lowest interest rate. The interest has a huge impact on the overall borrowing costs of the consolidation loan.

- Check fees and other costs. Borrowers must check any fees associated with the loan, such as origination fees or prepayment penalties. These borrowing costs impact the overall cost of the loan and must be considered when comparing options.

- Review repayment terms. Borrowers must review the repayment terms offered by each lender, including the length of the loan and any options for deferral or forbearance. Choose the loan with repayment terms that best meet their needs and budget.

Applying For Loan Consolidation

The process of applying for a consolidation loan seems daunting, but it is generally a straightforward process. Borrowers only need to gather all the necessary documents, compare loan consolidation options, and fill out the application form with accurate information about themselves and their current loans.

Lenders review applications after receiving them and provide feedback regarding the borrower’s eligibility for a consolidated loan. Consolidating payday and installment loans helps ease financial burdens by reducing monthly payments, lowering interest rates, and simplifying debt repayment into a single payment plan.

As a leading provider in the financial industry, our company is committed to helping individuals effectively manage their finances and overcome the challenges posed by payday and installment loans. With a strong presence throughout the United States, we have successfully assisted numerous clients in consolidating their loans and achieving financial stability. The following table presents a comprehensive list of American states where our company is actively operating, providing borrowers with reliable solutions and personalized assistance. Whether you reside in one of these states or are considering consolidation options, our experienced team is dedicated to guiding you toward a brighter financial future.

| AL / Alabama | AK / Alaska | AZ / Arizona |

| AR / Arkansas | CA / California | CO / Colorado |

| CT / Connecticut | DE / Delaware | DC / District Of Columbia |

| FL / Florida | GA / Georgia | HI / Hawaii |

| ID / Idaho | IL / Illinois | IN / Indiana |

| IA / Iowa | KS / Kansas | KY / Kentucky |

| LA / Louisiana | ME / Maine | MD / Maryland |

| MA / Massachusetts | MI / Michigan | MN / Minnesota |

| MS / Mississippi | MO / Missouri | MT / Montana |

| NE / Nebraska | NV / Nevada | NH / New Hampshire |

| NJ / New Jersey | NM / New Mexico | NY / New York |

| NC / North Carolina | ND / North Dakota | OH / Ohio |

| OK / Oklahoma | OR / Oregon | PA / Pennsylvania |

| RI / Rhode Island | SC / South Carolina | SD / South Dakota |

| TN / Tennessee | TX / Texas | UT / Utah |

| VT / Vermont | VA / Virginia | WA / Washington |

| WV / West Virginia | WI / Wisconsin | WY / Wyoming |

Repaying The Consolidated Loan

The costs of consolidation loans vary depending on the lender, loan terms, and the borrower’s creditworthiness. Certain lenders charge origination fees, prepayment penalties, or other fees, so it’s best to read the terms and conditions carefully before signing any agreement. Debt consolidation loans have interest rates ranging from 6% to 36%, according to Bankrate. The interest rates increase if borrowers fail to repay the loan on time.

| Interest Rates | Scenario |

|---|---|

| 6% | Excellent credit score, low debt-to-income ratio |

| 12% | Good credit score, moderate debt-to-income ratio |

| 18% | Fair credit score, high debt-to-income ratio |

| 24% | Poor credit score, high debt-to-income ratio |

| 30% | Bad credit score, very high debt-to-income ratio, credit card debts |

| 36% | Very poor credit score, extremely high debt-to-income ratio, significant credit card debts |

The table above shows different interest rates for debt consolidation loans based on credit scores, debt-to-income ratios, and annual percentage rates related to credit card debts.

- Scenario 1 – A borrower with an excellent credit score and low debt-to-income ratio will likely receive a lower interest rate, such as 6%.

- Scenario 2 – A borrower with a good credit score and moderate debt-to-income ratio receives a higher interest rate, such as 12%.

- Scenario 3 – A borrower with a fair credit score and high debt-to-income ratio receives an even higher interest rate, such as 18%.

- Scenario 4 – A borrower with a poor credit score and high debt-to-income ratio receives an interest rate as high as 24%.

- Scenario 5 – A borrower with a bad credit score and a very high debt-to-income ratio receives an interest rate as high as 30%.

- Scenario 6 – A borrower with a very poor credit score and an extremely high debt-to-income ratio receives the highest interest rate, such as 36%.

There are ways to avoid extra fees and high-interest rates of consolidation loans. Borrowers are free to set up automatic payments and loan refinancing.

Automatic Payments

Automatic payments are a feature offered by many lenders that allow borrowers to schedule their loan payments to be automatically deducted from their bank account regularly. It is a convenient option for borrowers who want to be sure they never miss a payment, as the payments are made automatically and on time. Certain lenders offer a discount or other incentive for borrowers who sign up for automatic payments, which helps reduce the overall cost of the loan.

Loan Refinancing

Another option for repaying a consolidated loan is through loan refinancing. Refinancing involves getting a new loan with better terms and using it to pay off existing debt. It results in lower interest rates, smaller monthly payments, or both. But note that refinancing extends the length of the repayment period and increases the total amount. It’s best to weigh the potential benefits against the costs before deciding if refinancing suits the circumstances.

Conclusion

Many individuals face financial difficulties in today’s uncertain economy and rely on payday and installment loans to cover their expenses. Consolidation of loans is an effective solution for simplifying repayment schedules, lowering interest rates, and reducing fees. But careful planning is necessary to determine if consolidation is the right option and to find the best loan consolidation option for one’s financial situation.

Applying for a consolidation loan is straightforward and helps borrowers save money and ease their financial burden. Understanding the benefits and drawbacks of consolidation loans, comparing consolidation solutions, and reviewing repayment terms are key to successfully consolidating payday and installment loans.

Frequently Asked Questions

What is the difference between payday loans and installment loans?

Payday loans are due in full on your next paydate. Installment loans are repaid over multiple scheduled payments with longer terms.

Can I consolidate payday loans and installment loans into a single payment?

Yes, debt consolidation can combine multiple loans into one payment. Fees may apply. Check with each lender first before pursuing consolidation.

What are the benefits of consolidating payday and installment loans?

Potential benefits are simplifying payments, lower monthly costs, improved credit score, and avoiding default or late fees on the original loans.

What are the common methods for consolidating payday and installment loans?

Common options are taking a consolidation loan from a bank, using a credit counseling agency, or working directly with the lenders to refinance the debt.

Are there any risks or drawbacks to consolidating these types of loans?

Risks include acquisition fees, higher interest rates on new loan, immediate payment requirements, and extended loan terms leading to more interest costs.