We sometimes have questions to ask about payday loans and debt consolidation. Payday loans are a quick way to borrow cash for unexpected expenses. These short-term loans can be repaid on the next payday.

Although this may seem like a great way to solve cash flow problems, payday loans can quickly become problematic if borrowers do not repay them within the first pay period. It can lead to a debt cycle and create a need to consolidate these loans with a personal loan. The credit check required by some lenders and credit unions can impact your financial situation.

Credit and payday loans: What they can do to your credit

Lenders don’t report payday loans to major credit reporting agencies. If the borrower defaults, it is debt collectors that take over. Once the collection agency has purchased the debt, it can report it to credit agencies. It can impact your ability to secure a single loan with better terms or enroll in a debt management plan to handle credit card debts.

Payday lenders may file lawsuits against borrowers if they fail to repay the loan. Non-payment of loans may be grounds for lawsuits by payday lenders. Working with a credit counselor to create a debt management program and improve your financial situation is important. By consolidating multiple payday loans into a single unsecured debt, you can reduce the monthly payment and have a more manageable repayment period. A lower annual percentage rate and a longer loan term can help you escape the debt cycle.

This judgment could show up on your credit report. It could negatively impact your credit score. Other lenders could use this information to report your history of payday loans and other types of loans. Credit bureaus may also consider this information when evaluating your credit utilization ratio.

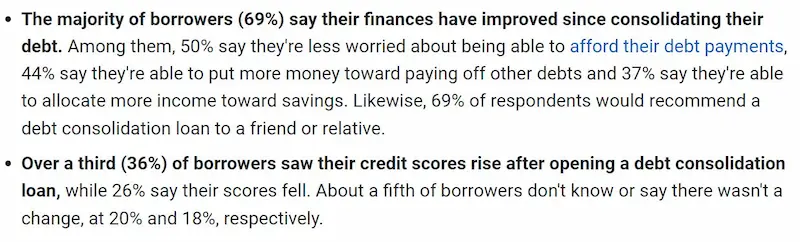

Here are some statistics about how payday loan consolidation can hurt your credit score:

| Impact | Percentage |

|---|---|

| Hard credit inquiry | 5-10 points |

| Late payments | 100 points or more |

| Average credit score drop | 10 points |

There are many options for payday loan relief

Consolidating your debt can make it easier to pay off any payday loan debts, student loans, unsecured loans, or any other types of debt. But “debt consolidation” can also refer to two things. Both should not impact your credit score, but one will. Another option for relief is using a balance transfer credit card to help manage your current debts, but keep in mind the potential balance transfer fees involved.

What is the difference between debt settlement and consolidation?

A debt consolidation option, such as a debt consolidation loan, is a way to consolidate debts. A bank will grant one larger loan to pay off all the other loans. Consolidation loans have a lower interest rate, but they are generally available for a longer time. It can help you avoid a debt trap and create a manageable payment plan. On the other hand, a late payment on your consolidated debts may still negatively affect your credit score. It’s crucial to explore various debt consolidation alternatives to find the best fit for your financial situation.

Consolidated loans offer a shorter period for repayment and lower interest rates than traditional loans. Consolidated loans will make it easier to manage your debt load through a single payment. Consolidation loans can show you how much debt you paid in full, according to credit reports.

Many people consider debt consolidation part of a debt settlement plan. Consolidation involves making one payment to a company and distributing the amount to your creditors. There are different types of debt consolidation, such as obtaining an online lender, using a balance transfer card, or benefiting from favorable terms with an average interest rate and annual interest rate adjustments.

A debt settlement company can negotiate a lower settlement than the original agreement during the introductory period.

Choose a Reputable Company

Do your research before you sign up for a debt consolidation plan. It is crucial to understand the type of program or loan it is. Evaluate your monthly income and ensure you have a sufficient income to cover the borrowing costs.

It is your responsibility to ensure that you make payments on time. Make sure to contact a nonprofit credit counselor for proper guidance and assistance throughout the loan application and application process.

Tax refund cash advance emergency loans 2023 near me may seem like a quick solution to financial troubles, but it’s important to understand the potential consequences. First and foremost, these loans often come with high-interest rates and fees that can lead to a vicious cycle of debt. Additionally, taking out another loan could worsen your situation if you’re already struggling with debt and considering payday loan consolidation or other debt-relief options.

For those with bad credit or poor credit, a tax refund cash advance could further damage your credit history, as payment history is a major factor in determining credit rating. If you cannot make timely loan payments, your credit may continue to decline, limiting your access to more favorable types of credit or secured loans.

When seeking an alternative loan, it’s crucial to take the time to plan ahead and realistically assess your ability to manage time payments without creating further financial stress. An option worth considering is setting up automatic payments to ensure on-time payments and work towards a healthier credit score. Additionally, strive to obtain a loan with a manageable payment schedule to avoid falling behind on payments and worsening your financial situation.

You must assess any limited time offer related to tax refund cash advance emergency loans. Check its long-term impact on your financial well-being. It’s essential to carefully consider your options and make informed decisions to break free from the cycle of debt and improve your overall credit history and payment history.

Frequently Asked Questions

Does payday loan consolidation negatively impact my credit score?

Payday loan consolidation can negatively impact your credit temporarily due to hard inquiries and lower account mix. Impact should lessen over time as balances decrease.

What are the potential credit consequences of payday loan consolidation?

Potential consequences include lower credit scores, closing accounts lowering total available credit, and new delinquencies if unable to repay the consolidation loan.

How can I protect my credit when considering payday loan consolidation?

Minimize hard inquiries by comparing rates from just a few lenders. Also maintain on-time payments and keep credit card balances low during the consolidation process.

Are there any alternatives to payday loan consolidation that won’t hurt my credit?

Alternatives like debt management plans through nonprofits, credit counseling, debt settlement, or bankruptcy may be less damaging to your credit than payday loan consolidation loans.

What steps can I take to rebuild my credit after payday loan consolidation?

Make all payments on time, maintain low card balances, dispute any errors, and let your credit history age. Don’t take on new debt immediately after consolidation.